The canary in the coal mine is an often-used metaphor to describe an impending downfall in the stock market. This article will cover three distinct canaries:

- Falling Liquidity in the Repo Markets

- Increased Incidences of Fraud

- Circular Investing

The Origin of the Metaphor

Since the 1890s, coal miners would walk into a mine shaft carrying a canary in a small cage. The canary was known to have a hyper-efficient respiratory system and would fall victim to methane and carbon monoxide before humans. If a coal miner noticed the canary stop singing and start to struggle, they would immediately extinguish their lamps and run out of the shaft.

While not a guarantee, these three major indicators show signs that the stock market is about to turn negative.

Falling Liquidity in the Repo Markets

Most investors are trained to focus their attention on revenue and earnings. In fact, for the last 50 or more years, investors have been led to believe that stocks are priced efficiently and that your return is a function of the asset class you are invested in—that changes in stock prices only come with changes in information.

There is one critical flaw to this theory: investors also buy or sell based on liquidity. If investors have more money, or feel like they have more money, they will continue to buy stocks. If they have less money, or feel like they have less money, they will sell stocks. You may have experienced a moment when you received a windfall and decided to purchase stocks. Others may have had an adverse event due to health, job loss, divorce, taxes, or death and needed to sell stocks. These are called liquidity-driven events and can adversely affect stocks.

Banks are also affected by liquidity needs. When loans begin to fail, as recently seen in loan failures from companies like First Brands Group and Tricolor Holdings, banks become hesitant to take on risk and to make loans in the repo market to other banks. This makes it harder for banks who need overnight funding to meet liquidity requirements. When banks cannot borrow money quickly, they may be forced to sell assets quickly, sometimes at a loss, to meet withdrawal demands from customers. This can cause a run on the bank and consequently a bank failure. This is what happened to Silicon Valley Bank and Signature Bank.

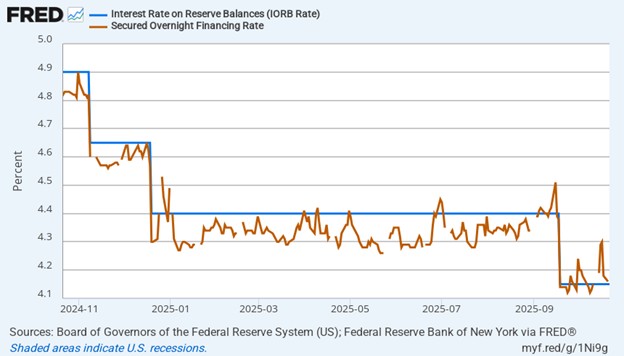

Evidence that the warning light is flickering on the repo market is the spread between the Interest On Reserve Balances (IORB) and the Secured Overnight Financing Rate(SOFR).

When the SOFR spikes higher than the IORB, it indicates that banks are charging excessive amounts to loan money, exceeding what they can receive in interest on their reserves at the Fed. This is due to the lending banks’ concern about the credit quality of the borrowing banks. This SOFR rate can spike dramatically, as seen in September of 2019 when rates went from around two percent to more than eight percent.

Higher SOFR rates and large drawdowns from the Federal Reserve’s Standing Repo Facility should be watched closely to judge the credit quality of the banking system. If banks won’t lend to each other, what is the probability they will create new or refinance marginal loans?

Increased Incidences of Fraud

As investors become more enthusiastic and more optimistic, they become more susceptible to fraud. The adage, “Everyone is making money at it, so it has got to be good,” becomes the heuristic for investing. They blindly invest out of fear of missing out (FOMO). This is when fraud starts to reach its pinnacle and is typically discovered when markets start to correct. For example, last week Zions Bancorporation discovered a $60 million loss in an investment related to loan fraud. Western Alliance began legal proceedings against another institution for loan fraud. Tricolor and First Brands filed bankruptcy from failed loans that allegedly contained missing funds, double-pledging of collateral, and opaque off-balance sheet financing. JP Morgan just wrote off $170 million in loans, prompting Jamie Dimon to state, “And I probably shouldn’t say this, but when you see one cockroach, there are probably more. Everyone should be forewarned on this one.”

A couple of years ago, private equity started pushing private credit funds to investors. These funds are called Non-Depository Financial Institutions (NDFIs). The NDFIs borrow money from banks and then lend to institutions or funds that cannot get traditional bank loans. It is my opinion that most of these loans were given to other private equity funds and companies that were having liquidity problems. This was illustrated in detail in my letter to investors titled, “Will Private Equity Lead the Next Market Collapse.” Lending fraud is a strong indicator of a market top. Think back to 2007–2008 and all the cockroaches found in the mortgage market.

Circular Investing

Henry Ford once famously said, “You can’t build a reputation on what you are going to do.” Circular investing is when a tech giant invests stock or cash in a startup client in exchange for a massive, long-term service contract. This is a defining feature of the modern cloud economy.

Here are a few examples:

The Amazon-Anthropic Deal

Amazon Web Services (AWS) agreed to invest up to $4 billion in Anthropic, the creator of the Claude AI model and a top competitor to OpenAI. In exchange, Anthropic has made a long-term commitment to use AWS as its primary cloud provider. Anthropic also agreed to use AWS’s custom-designed AI chips (Trainium and Inferentia) for building, training, and deploying its models. The AWS investment was a strategic combination of cash and cloud computing credits, with a substantial portion structured as credits.

The Microsoft-OpenAI Partnership (The Originator)

Microsoft has made a series of investments in OpenAI, totaling a reported $13 billion. In return, OpenAI signed an exclusive, long-term contract to run essentially all its workloads (training, inference, and API services) on Microsoft Azure cloud infrastructure. Microsoft’s total investment in OpenAI was made using a combination of cash and Azure cloud computing credits, with a significant portion allocated to the latter.

OpenAI – Oracle Deal

OpenAI agrees to purchase $300 billion in cloud computing power from Oracle over five years. Oracle will borrow money to build AI data center projects based on the hope that OpenAI can grow its current annual estimated revenue of $10 to $13 billion to the required $60 billion per year to pay for the projects. This deal also created an ancillary benefit to Nvidia and other chip makers who will sell to Oracle the tens of billions of dollars of AI chips needed for the buildout.

While these deals give the appearance of strong future growth, they are all susceptible to continued consumer demand in AI and the profitability of companies providing the services. Furthermore, there will also be conflicts of interest as companies like OpenAI try to negotiate their exclusivity with current providers. Neither OpenAI nor Anthropic are currently profitable. They, along with AWS, Oracle, and Microsoft, are making huge bets on their profitability.

This is reminiscent of companies like Global Crossing and WorldCom who took on hundreds of billions in debt to aggressively lay fiber optic cables worldwide. This was a bet that internet traffic would grow so fast that they would be able to sell all that capacity to the new dot-com companies. When the internet bubble burst, these companies fell into bankruptcy.

Conclusion

While the canary might be breathing easily today, many high-profile investors are signaling alarm. Warren Buffett has approximately 33% of his portfolio in cash. Jamie Dimon of JP Morgan recently issued warnings about the stock market; one of his major points is complacency and excessive optimism. Brian Moynihan of Bank of America expressed his concerns about the increased odds of a recession due to a changing economy. Howard Marks is urging his investors to pick up more defensive stocks. Larry Fink of Blackrock and David Solomon from Goldman Sachs are cautioning investors about potential market turndowns due to underlying economic and geopolitical risks.

Investors who have participated in the riskiest parts of the market have been rewarded in recent years. Those investors who have invested in the defensive parts of the market have lagged behind. While the last three years have been a lottery winning event for risky investors, one major correction could wipe out all recent gains, as we saw in the market turndown in 2000, which took many years to recover.